Homeowners

Insurance

Get a free homeowners insurance quote and protect your home now.

Call Now: (866) 845-5337

Compare homeowner’s insurance quotes for your property

Securing homeowner’s insurance is a critical first step to protect your investment from all kinds of unforeseen events and disasters such as fire, accidents, frozen pipes, vandalism, theft and even volcanoes.

Choosing the best home insurance for your property can save you thousands of dollars over the course of your mortgage, making it important to compare the top providers for the best deal.

Save yourself the hassle and input your zip code above to instantly compare homeowners insurance quotes and secure the best home insurance for your property.

When you shop for home insurance quotes online, you will notice that standard policies offer four essential coverage types. Here are some basic definitions to help you understand the protections they provide.

This type of home insurance offers protection against any losses to your home or any other physical structures on your property (doghouse, treehouse, henhouse, guest house, driveway, etc). Dwelling coverage typically protects from losses caused by:

It doesn’t cover damage from floods, earthquakes, landslides, war, and other perils. If you want extra coverage, you can upgrade your policy. When you compare house insurance policies, make sure to check the full list of covered perils.

This type of homeowners insurance helps pay for the loss or damage of personal belongings like furniture and clothing, to a limit. Personal property damage is off-premise coverage; if someone steals your phone while you are out at a restaurant, you will be covered.

Most insurance companies will offer enhanced coverage for valuables like antiques, fine art, and electronic equipment—but they may need an appraisal.

This insurance covers fees if the policyholder or the people living in the home are responsible for injuries or damage. For example, if a tree limb falls on a visitor in your yard and it is determined that the injury was caused by negligence, you will receive money to cover the costs of legal fees, settlements, and more.

Generally, the cost comes to around 50% to 70% of your dwelling coverage. As with personal property damage, coverage extends outside of your home; you won’t have to pay out of pocket if you damage someone else’s property. If you have assets worth more than the policy limit, it may be wise to purchase excess liability coverage.

Temporary living expenses coverage helps you pay living costs if you are displaced due to a covered peril. This part of the policy pays for rent, lodging, meals, and other expenses you face while your home is being repaired.

The limits and limitations on your temporary living expenses won’t affect the amount of money available to restore or rebuild your home.

Additional living expense (ALE) typically covers you if you rent out part of your home as well. It imburses you for rent that your tenant would have paid you if your home wasn’t damaged. ALE is usually around 20% of the amount of dwelling coverage.

Homeowners insurance coverage applies to the owner/occupant of a dwelling such as a home, condominium, apartment, or multiple unit dwelling (residence must not exceed four families). The house must be solely used as a residence. However, you won’t be excluded from coverage if you have an office, school, or studio in your home used for business.

The home doesn’t need to be your primary residence. Seasonal homes, second homes, and homes under construction are all eligible for insurance. Homeowners’ insurance does not cover new homes under construction.

Most companies will give you a choice between two homeowners coverage options for how the amount of your settlement is calculated.

Replacement costs – covers the full cost of replacing, repair, or rebuilding your home to its original condition. If you need to replace a marble-tiled floor, it would cover the marble floor’s cost instead of the lower cost of ceramic tile.

Actual Value – covers the depreciated value of the cost of your property at the time of the loss. For example, the actual value you receive for a 5-year-old laptop will be much less than it would cost to replace it.

Replacement cost policies usually have higher premiums than actual value policies. While less common, some policies will allow you to determine your settlement based on repair costs.

Typical homeowners insurance deductibles range between $500 to $2500 for any claim. You will always have to pay this deductible before receiving a settlement for dwelling and personal property loss. However, not all types of coverage require a deductible.

A higher deductible will slightly reduce your monthly premium, but you will have to pay more out of pocket when it’s time to file a claim.

Getting peace of mind doesn’t have to be a chore. Want to get the best homeowners insurance quotes for comparison? With over 25 years of dedicated service to homeowners across the country, we have the knowledge and connections to help you find a policy that addresses all your financial needs and concerns.

Getting our free online home insurance quote is as easy as filling out your ZIP code and few button clicks. Ensure that pop-ups are enabled in your browser; otherwise, it may block our insurance application windows.

Please have the following information ready before you compare homeowners insurance quotes:

Remember that online homeowners insurance quotes are not binding. Insurance underwriters consider many different risk factors to determine your eligibility and your premium. Some key factors include:

Home features and condition – things like your home’s structure and the construction materials will affect your insurance cost. For example, premiums for houses built with brick frames are usually lower than homes built out of more flammable material like wood.

The age and condition of your home – older homes cost more to insure than new homes because they tend to require more repairs and upgrades. Properties in disrepair will also come with higher premiums than houses that are in good condition.

Location – coastal properties are riskier to insure than inland homes because there is a greater chance of natural disaster. Houses in areas susceptible to wildfires and damage from falling trees will also carry higher premiums.

If your home is located close to the fire department or has a fire hydrant in your front yard, this may help reduce your premium because you have a lower risk of fire damage. Low crime rates can also give you a lower premium due to the reduced risk of theft.

The state where you live also plays a significant role in your homeowners insurance rates and coverages. Explore more about homeowners insurance factors within your state.

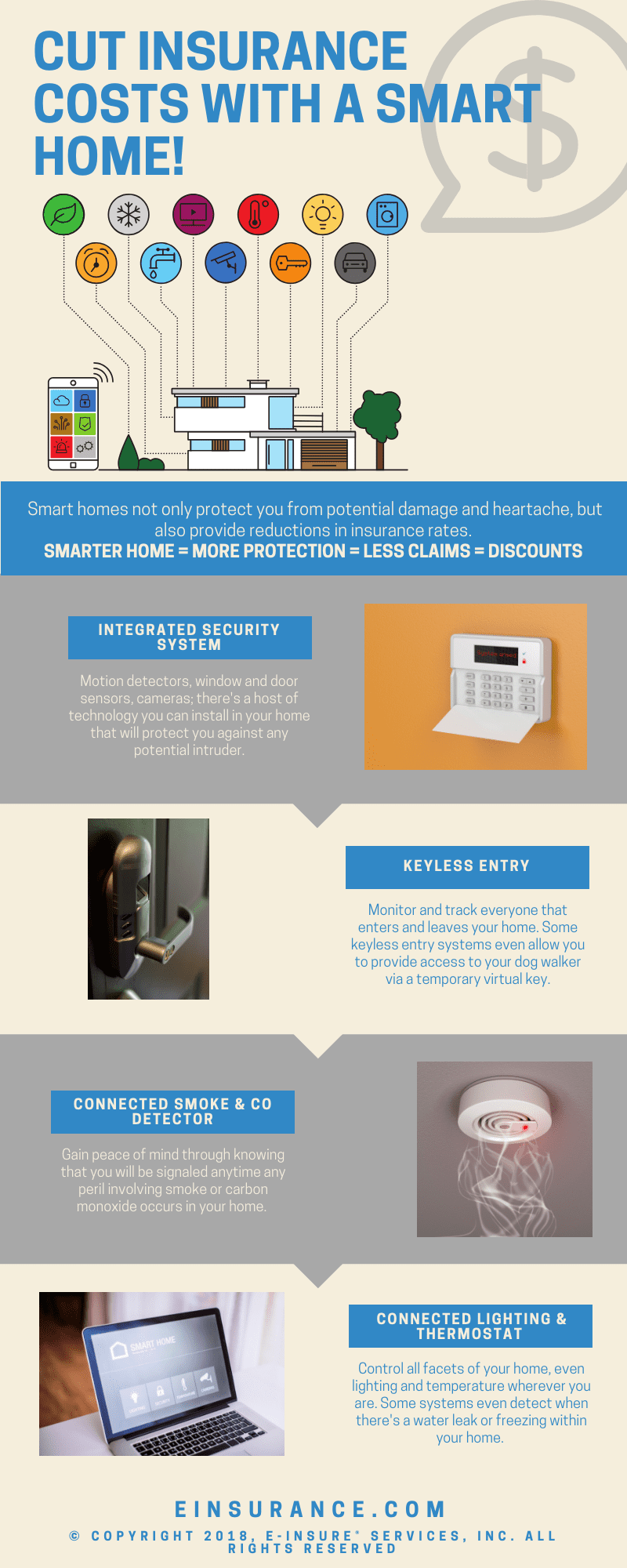

Home security – protective security measures like alarm systems, security cameras, video doorbells, and deadbolt locks will help determine the insurer’s likelihood that you will file a claim.

Claims history – this includes the type of claim you filed for and the number of claims you’ve filed in the past. If you have never filed a claim with the insurer, you are more likely to pay less than someone who has filed multiple claims.

Personal attributes – smokers can expect to pay 20% more for homeowners insurance than non-smokers. Bad credit can also come with higher premiums.

Credit score – most states will consider your credit score during their risk assessment, giving you higher quotes for lower scores. Massachusetts, Maryland, and California are the only states that do not allow insurance companies to factor in your credit score when they calculate their quotes.

A standard policy will cover your home and other structures on your property to a limit. The amount you need depends on how much it will cost to rebuild your home. It’s important to understand the limitations and boundaries of the policy you are looking at to get the right coverage. Some things to consider are:

We recommend that you compare homeowners insurance quotes online from at least three different companies to find the best homeowners insurance. Data from homeowners insurance report for 2020 released by NAIC in December 2022 showed that homeowner insurance’s average annual cost was $1,311 in 2020, up 8.26% compared with 2019.

Here are a couple of things you can do to get discounts on your policy without sacrificing coverage:

Learn more about how you can save money on homeowners insurance.

After you have received an instant home insurance quote, you should do some research on the insurers. J.D. Power Research and the NAIC are two reputable sources you can use to determine an insurance company’s credibility.

Yes and no. You can own a home without homeowners insurance, but it is a requirement to finance a home. After you pay off your mortgage, you will no longer be required to carry homeowners insurance. However, you won’t be protected if anything unexpected happens down the line, which can be risky.

Additionally, if you purchase a condo or cooperative unit, you may be required to purchase homeowners insurance. Make sure to check with your HOA to see if home insurance is necessary.

It helps to have things in order so you can avoid any unexpected fallouts when it comes to your coverage. Here are some helpful things you can do:

It’s easy to find homeowners insurance, but it’s a challenge to find insurance that covers all of your needs at the best price. You may be surprised at how much you can save when you compare house insurance quotes with us.

All you need to do is provide some basic information about yourself and your home, and we will handle the rest. Get started now with a free online homeowners insurance quote.