Renters Insurance Quotes

Rest Assured Rent with Renters Insurance

Renters Insurance covers your personal property (clothing, jewelry, computer hardware/software, electronics, furniture and other valuables) if you rent a room or an apartment. Typically, it also covers against personal liability (up to some specified amount) for those who are injured in your rental unit.

Renters Insurance quotes typically covers the possibility of damage from things like fire, smoke, lightning, wind, hail, explosions, riots, water from pipes, theft, and vandalism. It may also cover any costs associated with living somewhere else while your unit is being repaired.

What Renters Insurance Is Not

Renters Insurance is not a Homeowner’s Policy, and usually costs significantly less.

People who operate a business out of their apartments may need to purchase additional commercial insurance to protect their business interests.

Renters Insurance doesn’t protect you in the event that your landlord refuses to refund a portion of your security deposit. This is a contractual issue, not an insurance one.

Who Needs Renters Insurance?

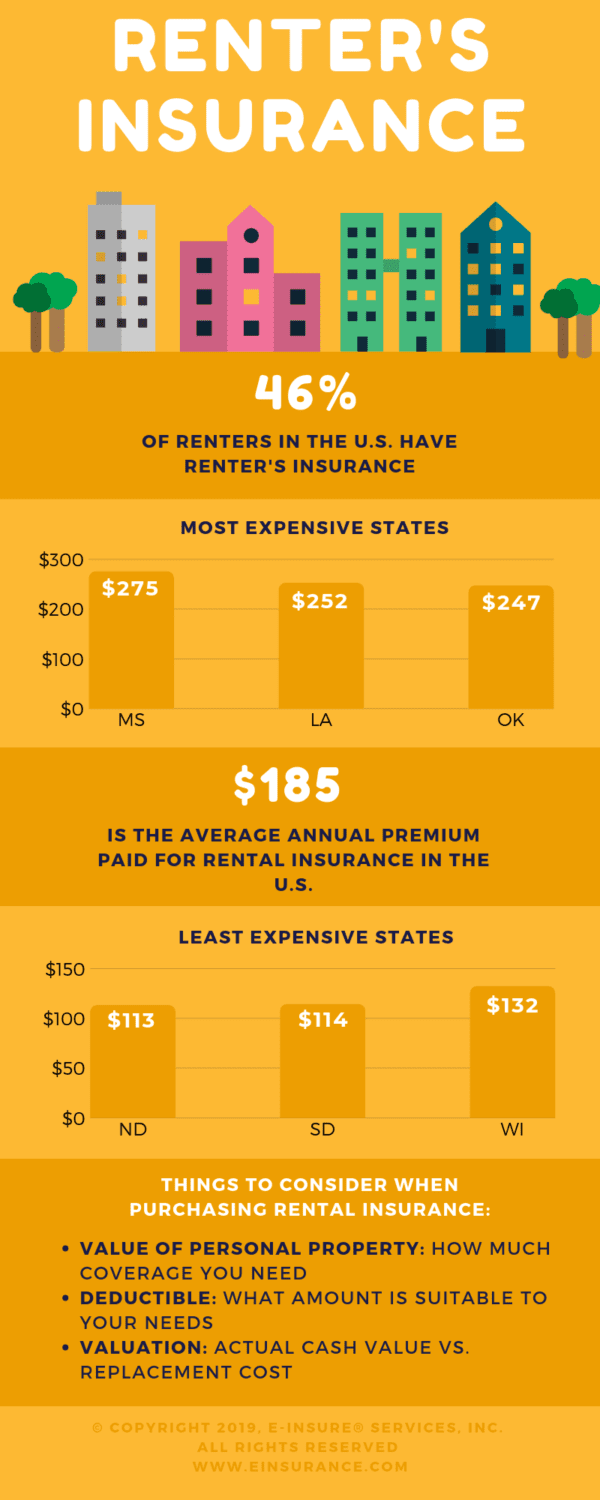

Anyone who rents living space should consider Renters Insurance (although fewer than 25% actually have a policy!). It is especially important if you have valuable items like antiques, artwork, memorabilia, jewelry, or expensive electronics that would be difficult to replace should they be damaged or stolen.

Students living away from home should consider Renters Insurance, as only a portion of their property may be covered by their parents’ homeowners’ policy. This is especially the case with students living in off-campus housing, fraternities, and sororities.

Things To Think About

The most important consideration is whether the renters Insurance quotes covers actual cash value or replacement cost of the damaged or stolen property. Actual cash value is what the item is worth today; replacement cost is what you’d have to spend to get a new one.

Like most types of property insurance, Renters Insurance may not cover loss due to floods and earthquakes. Additional coverage for these events may need to be purchased as a rider or a separate policy.

The Renters policy may limit losses for certain items like cash, computers, jewelry, silverware, furs and firearms. You may need additional coverage for exceptionally expensive items.

If you have a waterbed (and you live above someone else!), consider a policy that covers against waterbed leaks.

Two final considerations. First, does the policy cover damage or loss to your personal property when away from home? Second, if you’re a pet owner, does this affect your Renters Insurance premium? Owners of certain dog breeds (Rottweilers, Pit Bulls, Dobermans) may not qualify for liability coverage, or may have to pay a much higher premium.

Relevant EINSURANCE Journal Content

4 Reasons To Buy Renters Insurance

Renters Insurance Vs. Landlord Insurance: What They Do & Don’t Cover

What Kind of Renters Insurance Policy Do You Need?